Nigeria Tax Calculator

March 2, 2026, 10:37 am

A lot of confusion exists over the new tax regime in Nigeria. This article aims to make it simple and easy for citizens to know and calculate their tax responsibility

What is Taxation?

Taxation is the obligatory, non-negotiable collection of financial charges from persons and businesses by a government to pay for public expenditures such as infrastructure, defense, and social services.

Individuals and businesses generate revenue from three key sources: rent, profit, and wages. As a result, all taxes must eventually be paid from one of these three different streams of revenue.

Tax Reforms in Nigeria

The new tax regime in Nigeria came about via the 2025 Tax Reforms. This reforms mark a transformative chapter in Nigeria’s fiscal landscape. The overhaul of existing legislation is designed to modernize and simplify the country’s tax system, with the aim of enhancing revenue generation and promoting equity.

The newly enacted laws as an outcome of the reforms are:

a) The Nigeria Tax Act

b) The Nigeria Tax Administration Act

c) The Nigeria Revenue Service Establishment Act

d) The Joint Revenue Board (Establishment) Act

Nigeria Tax Act (NTA)

The NTA consolidates the country’s tax framework and seeks to align Nigeria’s tax system with international best practices while addressing local economic realities. The NTA represents a landmark overhaul of the country’s fiscal architecture, unifying and modernizing tax rules across the petroleum, electricity, and mining sectors.

By repealing outdated laws and amending the Petroleum Industry Act, the government has created a transparent, predictable, and investor-friendly tax regime. The Act’s alignment with the Electricity Act of 2023 underscores a strategic push to reform the power sector, encouraging private investment, efficiency, and sustainability.

Nigeria Tax Administration Act (NTAA)

The NTAA governs tax administration across all government tiers (federal, state and local) and consolidates administrative provisions from multiple existing tax laws.

The Nigeria Revenue Service Establishment Act (NRSEA)

The NRSEA replaces the Federal Inland Revenue Service (Establishment) Act (FIRSEA), 2007. It establishes the Nigeria Revenue Service (NRS) as a new federal body responsible for administering and accounting for all taxes and revenues under laws enacted by the National Assembly.

The Joint Revenue Board Establishment Act (JRBEA)

The JRBEA provides a comprehensive institutional framework to enhance the efficiency of revenue administration in Nigeria. The law creates the Joint Revenue Board (JRB), which replaces the existing Joint Tax Board (JTB). Unlike the JTB, which mainly served as a platform for dialogue and policy coordination among tax authorities but without enforcement authority, the JRB has a stronger mandate.

It is now responsible for harmonizing and coordinating tax administration across federal, state, and local governments. This helps to reduce conflicts and inconsistencies in the tax system. It is also vested with the authority to resolve disputes between federal and state revenue authorities, as well as among state revenue authorities.

Tax Payment in Nigeria

In Nigeria, businesses and persons are eligible for tax payment to the relevant authorities. Taxes that persons or individuals pay are called personal income tax while taxes paid by businesses are classified under company income tax

Use of Taxpayer Identification Number (TIN)

The NTAA mandates that all financial service providers—including banks, insurance companies, stockbrokers, and other related entities—ensure that every taxable person, whether an individual or a business, supplies a valid TIN. This comprehensive approach underscores the government’s commitment to fostering transparency, improving tax compliance, and mitigating illicit financial flows across the entire financial services ecosystem

Nigeria Tax Calculator

Since two major entities (businesses and persons) pay tax in Nigeria, let us start with the calculation of taxes paid by businesses or companies

Company Income Tax Calculations

All companies will be taxed based on the profits that their operations generate. Profits for companies can be calculated by knowing the company’s Turnover, Cost of Sales and Expenses.

Turnover is the total revenue (or gross sales) that a company earns from selling goods or services over a given time period.

Cost of Sales is the direct and variable costs attributable to the production of goods or delivery of services sold by a company. It includes raw materials, direct labor, and manufacturing overhead

Expenses are charges incurred during the everyday operations of a business. These include selling, general, levies and administrative expenses, as well as the depreciation and amortization of fixed assets.

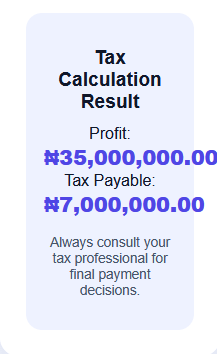

When these indices are known, it’s straightforward to calculate a company’s profit. A company’s profit is the deduction of cost of sales and expenses from turnover

In Nigeria, the tax rate companies will now pay depends on the level of their turnover. These rates are given below:

- 0% (if annual turnover is less than

N25,000,000) - 20% (if annual turnover is higher than

N25,000,000 but less thanN100,000,000) - 30% (if annual turnover is higher than

N100,000,000)

To help you simplify and see your company’s tax obligations, we have created a Company Income Tax calculator tool. This is how our company income tax calculator works

Go to our Company Income Tax Calculator

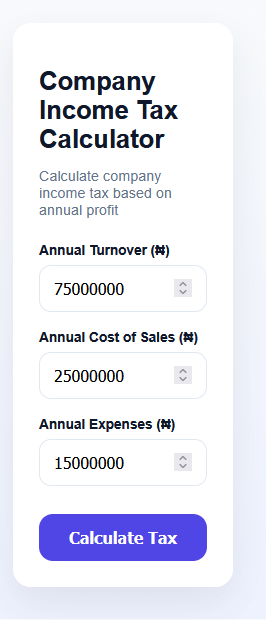

Enter your company’s annual turnover, cost of sales and expenses. For this demonstration we have entered N75,000,000 for annual turnover, N25,000,000 for annual cost of sales and N15,000,000 for annual expenses.

Click the Calculate Tax button

You will be given a rough estimate of what your company will pay as tax

Personal Income Tax Calculations

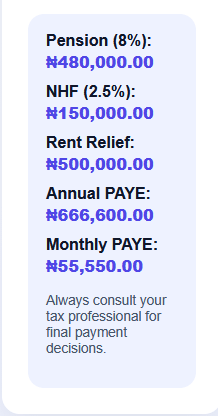

The taxes persons pay in Nigeria fall under the PAYE (pay-as-you-earn) category. Under the new Nigeria tax laws, certain deductions are allowable from your income before you are taxed.

Some of the deductions made from your salary before tax applies are pension, rent relief, housing fund, insurance etc. After these deductions have been made, what is left is your chargeable income from which tax is deducted.

These deductions vary per individual because no two person’s financial situation are the same. For example, Rent Relief is calculated at the lower of 20% of your annual rent paid, or ₦ 500,000. Your rent relief will vary from someone else based on where you live and the type of house you live in.

After these deductions have been made, your chargeable income is then taxed according to the table below:

| Chargeable Income Range | Tax Rate |

| 0 to |

0% |

| 15% | |

| 18% | |

| 21% | |

| 23% | |

| Above |

25% |

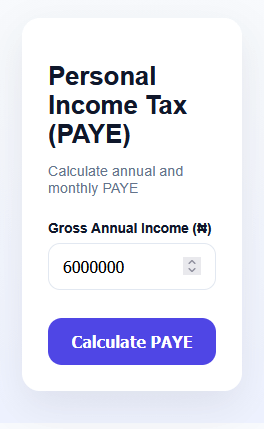

To help you see how you can know your personal income tax, you can use our Personal Income Tax calculator with the steps below:

Go to our Personal Income Tax Calculator Tool

Enter your annual gross income or salary which is your total yearly income or salary without any deductions. In this example, we have entered N6,000,000

Click on the Calculate PAYE button and you will be given a breakdown of all your deductions and tax payment.

Please keep in mind that our tax calculator tools (personal tax and company tax) are only intended to provide an informed guide. It’s advisable for both companies and persons to engage professional tax accountants for all tax filings and final payment decisions

Tax Actionable Insights

In light of the tax reforms introduced in Nigeria, below are some steps companies and persons can take to ensure that they don’t get into tax troubles:

1. Immediate registration and compliance— All taxable persons and entities must register for tax and obtain a Taxpayer Identification Number (TIN) to avoid substantial initial and recurring penalties. Awarding contracts to unregistered persons now attracts a significant ₦5,000,000 penalty.

2. Timely and accurate filing— Ensure all tax returns are filed accurately and on time. Delays or inaccuracies trigger escalating monthly penalties, which can quickly accumulate to substantial amounts.

3. Maintain Proper Records— Companies and individuals must keep and provide adequate records. Failure to do so results in immediate penalties and can hinder the ability to defend against further assessments or audits.

4. Enable Tax Technology and Fiscalisation— Grant access for tax automation and use the prescribed fiscalisation systems for VAT and other taxes. Non-compliance leads to high daily penalties and additional interest on tax due.

5. Deduct and remit taxes at Source— Entities responsible for withholding taxes must deduct and remit them promptly. Failure to do so results in a 40% penalty on the undeducted amount, plus interest and possible criminal liability.

6. Monitor and respond to information requests— Respond promptly to all tax authority requests for information. Non-compliance now attracts significant daily penalties.

Sources and References

- PwC, Nigerian Tax Reforms, 2025: Tax Insight Series and Sectoral Analysis

- Presidential Fiscal Policy and Tax Reform Committee

Share This Article: