Covid-19: From A Global Health Crisis To A Global Food Crisis?

August 5, 2020, 1:06 pm

As the world faces an unprecedented public health crisis in living memory in the form of COVID-19, this special feature examines the current and likely impacts of the pandemic – the “Great Lockdown” – with a focus on international food markets.

Covid-19: From A Global Health Crisis To A Global Food Crisis?

Such markets are not insulated from changes in the wider economy, therefore emphasis is placed on how broader economic shocks have, and can be, transmitted to food markets, notwithstanding the direct transmittable effects of the novel virus to the agricultural sector. In terms of required policy responses, much can be learnt from previous crises, especially the “Great Recession” culminating in 2009. It provides an informative benchmark on how to return market functioning to normality, even if contagion rates remain unchecked.

The big picture – what we can expect

With the new coronavirus spreading rapidly, the impacts of the COVID-19 pandemic on global agricultural and food markets are becoming increasingly apparent. The contours of these impacts are shaped by changes in macroeconomic environments, energy and credit markets, and importantly, input prices and prices in agricultural factor markets. Some of these shifts resemble those of the last global crisis – the Great Recession – and the lessons learnt can help target policy responses in addressing the challenges of the severe ongoing economic emergency.

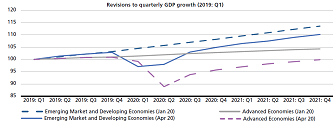

Not to detract from the global scale of the human tragedy from COVID-19, a leading indicator of the economic impact of the virus is that of GDP growth. The International Monetary Fund’s (IMF) most recent World Economic Outlook (April 2020) forecasts a global recession to the tune of a -3 percent annual fall in world GDP in 2020. This compares with a mere -0.1 percent reduction in 2009. The IMF expects global growth to rebound in 2021, with a yearly growth rate of 5.8 percent. It estimates the cumulative output loss in both 2020 and 2021 at USD 9 trillion. The Fund’s projections also suggest that no country group – rich or poor – will escape economic contraction, with high-income countries expected to experience deeper and longer-lasting recessions. Such has been the severity of the COVID-19 shock that the IMF has significantly downgraded GDP growth in a matter of months, as illustrated in the table below:

The newly projected economic environments are likely to unleash profound impacts on food demand, access to food and nutritional outcomes, well into next year. The big question is whether COVID-19 will lead to a full-blown global food crisis, resembling what the world experienced over the years 2007 to 2009.

Is there enough food currently available?

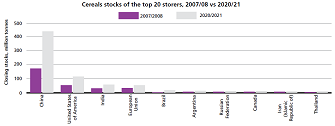

To set the all-important stage, a critical question is whether current global food supplies can satisfy food needs. One traditional indicator to guide this assessment is the amount of cereal stocks held globally, and their ‘liquidity’, that is whether they are made available for procurement on the international stage. At the beginning of the 2020 COVID-19 crisis, cereal stocks hovered around a multi-year high of about 850 million tonnes. In absolute terms, they were nearly twice as high as at the beginning of the 2007/08 crisis (472 million tonnes) and even relative to utilization, they had reached levels far above those registered in 2007/08. These high stocks should provide a solid buffer against adverse shocks such as, for instance, a bad weather event in the 2020/21 growing season. While important, absolute levels of stocks are not all that matters for buffer capacity. Equally significant is the distribution of stocks over countries, over exporters and importers, and notably, their concentration over major storers (few or many). Irrespective of the tradability or not of cereal inventories concentrated in a few major countries, the table below shows that many countries are better placed to distribute staples for domestic utilization from current stocks, compared with the last crisis.

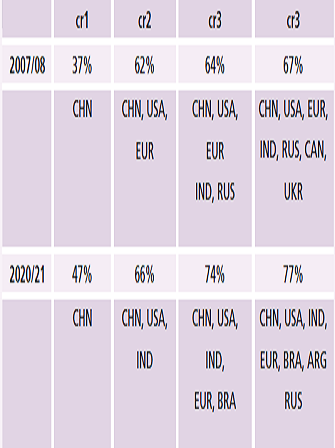

The table below summarizes the concentration ratios of cereal stock holders of the top 1, 3, 5 and 7 storers in 2007/08 and 2020/21.

All calculations are based on quantities. The figures show that the concentration of stocks across countries was already very high in 2007/08, but has further increased over time. A large share of stocks is not only in the hands of a few countries, but is also held by storers such as China and India, which have not been very responsive to global price signals in the past. Put into the context of the current crisis, the high stocks held globally may not provide as much buffer capacity as their absolute levels suggest in the case of a disruption in the global supply chains, caused, for instance, by a breakdown in bulk shipment facilities.

Falling price of internationally traded foodstuffs portend a boon for food security

The price hikes for basic foods on a global level made the 2007/08 crisis a particularly serious one. In addition to losing jobs and incomes, consumers also saw their purchasing power decline as food prices rose. The changes in international prices caused by the 2020 crisis are in stark contrast to the 2007/08 developments. Virtually all quotations for globally traded foodstuffs were in decline at the beginning of the year, and COVID-19 has since put further impetus to this trend, especially for sugar, vegetable oils and meat products. Barring major disruptions in the supply chains, the projected economic recession means that the trend of generally lower food prices could prevail throughout the current crisis. Lower food prices on international markets should also attenuate global food security concerns compared with the Great Recession. However, they cannot necessarily prevent local, national and international disruptions in food supply chains. Nor can they ensure that prices in local currencies do not see increases, given the often hefty depreciation of currencies against the US dollar.

Trade has an increasingly important role to play

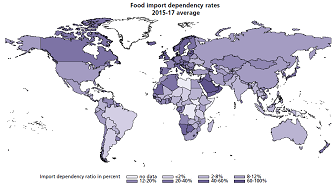

To put the importance of adequate global food supplies in further perspective, exporters of foodstuffs have an increasingly important role to play in meeting global food needs. Import dependency by countries on the international marketplace for food has steadily increased over time, and now stands on average at around 28% globally. However, as shown in the diagram below, there is a significant dispersion in the level of food import dependency, with some countries relying as much as 98 percent on the global markets for their food needs. Indeed, many countries that are traditionally heavily reliant on international markets are economically vulnerable, such as those situated in sub-Saharan Africa and South Asia, as well as Small Island Developing States (SIDS).

Their plight is particularly noteworthy given their dependence on foreign remittances, which are expected to decline sharply, while for SIDS, dependence on remittances, and to an even greater extent on tourism, increases their exposure due to the closure of international borders to visitors.

Greater diversification in agricultural trade equates to increased resilience

The degree of exposure of the global trading system to a crisis is also conditioned by the concentration of exporters and importers. A high concentration of exporters makes markets susceptible to logistical constraints or policy interventions (export restrictions) imposed by large players potentially jeopardizing access to food for importers.

Conversely, a high concentration on the import side could mean that a sharp reduction in import demand by one or two major importers could significantly affect prices and jeopardize revenue streams for exporters dependent on these agricultural exports.

A comparison of the pre-crisis situation in 2007–2009 and 2020 suggests that the concentration of agricultural trade has declined for many products on both the export and import sides, i.e. for many agricultural products. These are the bubbles in the lower left quadrant, i.e. all commodities for which the number of importers and exporters has risen, not declined. This means that, when moving into the 2020 crisis, more exporters and importers were participating in trade, which should make the global trading system for any given commodity more resilient to shocks, not more vulnerable.

Despite the greater diversity over importers and exporters in general, there are a number of noticeable deviations from this trend, i.e. commodities where either imports or exports, or both, have become more concentrated over countries. In addition to rice and palm oil, the most important product in this rubric are soybeans, for which China has become the dominant importer with a world market share close to 65%. Also, exports have remained in the hands of a few countries, notably the United States of America, Brazil, Argentina and, more recently, Paraguay. The generally greater diversification offers added resilience to the agricultural trading system, which should prove increasingly important, as the number of importing and exporting countries affected by the COVID-19 crisis rises.

Exchange rates matter for import capacity and trade competitiveness

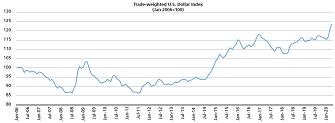

One of the immediate outcomes to the 2020 COVID-19 crisis has been an adverse change in exchange rates. The table below presents the trade-weighted US dollar index, which has climbed to an all-time high, suggesting that Low-Income Food-Deficit Countries (LIFDCs).

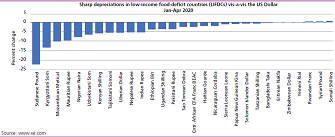

Also, as depicted in the chart below, LIFDCs could struggle to buy food even when international food prices are falling, especially those that do not have convertible currencies and are heavily reliant on foreign exchange reserves to procure goods on the international marketplace.

However, the strength of the US dollar has made non- US exporters more competitive and kept a lid on US dollar denominated commodity prices, notably maize and sugar, which were also affected by both lower energy prices and high export availabilities. However, over the medium term, the strength of the US dollar in conjunction with projected higher commodity prices could add to inflationary pressures in commodity exporting countries. It could also add to existing problems in servicing US dollar-denominated debts, which have seen a massive increase in recent years.

Current prices of energy, biofuels and agricultural inputs support food producers

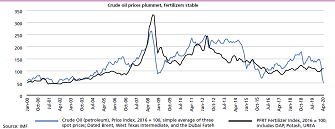

Agriculture is generally a highly energy-intensive industry, especially for modern and large-scale enterprises. Trends and absolute levels of energy prices in 2020 are radically different from those in 2007/08. In 2007–2008, Western Texas Intermediate (WTI) crude oil prices experienced a massive run-up, culminating by mid-2008 at levels close to $140/bbl, measured on a monthly average basis. In April 2020, by contrast, crude oil (WTI) prices had fallen below $20/bbl on a monthly basis, and even below $12/ bbl during intra-day lows.

In 2007/08, the rise in energy prices was so significant that it turned agricultural products into competitive feedstocks for the energy market, siphoning off increasing quantities of agricultural products from food markets into the biofuels market. The most direct effects were visible in the demand for bio-energy feedstocks, while the more indirect effects came through substitution on the demand side and competition for cropland on the supply side, which eventually lifted prices for all agricultural products.

The exact opposite set of drivers has been at work since the beginning of the COVID-19 crisis. The sharp decline in energy prices, as shown in the chart below, caused prices of ethanol and biodiesel to collapse and resulted, without any time lag, in strong declines in the demand for, and prices of, bioenergy feedstocks, such as maize, sugar and vegetable oils.

More generally, lower energy prices affect agricultural production costs through several channels. The direct impacts include lower costs of energy for all forms of mechanization, including power needed to till fields, for irrigation and for transportation. The indirect impacts are channelled through lower costs of energy-intensive inputs such, lubricants, pesticides and electricity while fertilizer prices have been contained. These generally lower input costs act as an automatic stabilizer for farm incomes, keep prices for basic foodstuffs under downward pressure and attenuate the direct impacts of the COVID-19 pandemic on food and agriculture.

Credit markets are tightening, debt soaring in lower-income countries

As in the case of the Great Recession, the 2020 crisis is also expected to have a negative impact on credit markets, with developing countries being hard hit, given their high indebtedness in foreign currencies, sharply depreciating exchange rates and low commodity and energy prices, which make it harder to service these debts. In response to the COVID-19 crisis, many central banks around the world intervened in lowering interest rates. Despite these moves, market rates for borrowing fresh capital have often risen, particularly in low-income countries. A Jubilee Debt Campaign reported that interest rates have on average risen by 3.5% points for low- and middle-income countries since mid-February, and that costs for new borrowing stood at 10%.

The build-up of private debt by non-financial corporations, e.g. private and public enterprises, which now amounts to nearly three-quarters of total debt in developing countries (a much higher ratio than in advanced economies), is seen as particularly concerning. According to the United Nations Conference on Trade and Development (UNCTAD), inherently volatile “foreign shadow financial institutions” have played a major role in fuelling this accumulation, such that around one-third of private nonfinancial corporate debt is located in low-income countries.

While debt vulnerabilities remain contained in the majority of Low-Income Developing Countries (LIDCs), some 40% of them currently face significant debt-related challenges. Nine out of 12 countries that moved from ‘low/ moderate risk’ to ‘high risk/in debt distress’ are located in sub-Saharan Africa.

With rising costs for capital, the impacts would also be felt in agriculture, notably capital-intensive forms of production. Credit markets could become an important channel of transmission, adversely affecting capital intensive agriculture. This would further deteriorate the commodity terms-of-trade for many commodity dependent LIDCs that have been under way since the last price hike in 2012.

Supply chain disruptions present a major hurdle

Agriculture and food supply chains are also labour-intensive (especially for high-value crops, meat and fish) and the effects of the Great Lockdown are bearing down heavily. Labour market shocks arise from mobility restrictions on workers, especially the migrant workforce, and the direct health impacts of COVID-19 are weighing directly on the ability of workers to produce, harvest or process food. The labour force is also affected by a deterioration of occupational health and safety standards. In addition, COVID-19 is having a major impact on moving food to domestic and international consumers, depending on the mode of transportation.

Bulk: The Baltic Dry Index, which is a benchmark measure for the cost of shipping goods around the world, is hovering at the lowest level in 25 years. For the first quarter of 2020, the index slipped more than 40% as the rapid spread of the new coronavirus led to shipping restrictions and weakened demand for dry bulk vessels. The index started to strengthen again in April 2020 as a gradual restart of industrial activity in China led to rising demand for shipping vessels.

Container and truck transportation: While bulk shipments have seen few disruptions and no upward pressure in prices, container and truck shipments are already affected by the COVID-19 outbreak. These affect mainly second-tier ports, transhipments to landlocked countries and truck transportation within large countries. For instance, shipments of tropical fruits from Southeast Asia, which are in season at this time of year (April–May), were disrupted through congestions at ports of Shanghai and Tianjin, leading to significant losses due to the perishability of the produce. As another example, cargo disruptions have been amplified by severe container shortages stemming from increased imports of pork in response to African Swine Fever. The closure of some wholesale markets due to quarantine measures has further impeded sales. Not just container shipments are under strain; there are also first reports about a lack of truck drivers due to quarantine restrictions, industrial action or actual illness. Strikes have been announced in several ports of Brazil and Argentina; if they materialize, this would be particularly disruptive given that April and May are the peak period for Brazilian soybean exports.

Air freight: The so-called ‘bellies’ of passenger jets are often used to ship high-value goods and foods, making up a small but important portion of cross-border trade around the world. As passenger traffic collapsed around the world, air freight followed suit. While capacity increased slightly on specialized cargo planes, the daily international capacity available from the bellies of passenger planes was 80% lower globally in the final week of March. At the same time, demand remained strong for air freight. As supply chains around ports continue to come under pressure, air transport remains a viable alternative for importers and exporters. As a result, prices for air freight, usually measured per kilogram or tonne of product, have risen. Relative to pre-crisis levels, estimates suggest that prices are up 20% to 30% across the Asia- Pacific region, and that for some routes, such as Hong Kong to Beijing, they may have jumped by about 50%.

All-in-all trade in food and agriculture likely to contract in 2020

Generally, lower incomes and supply chain disruptions suggests that total merchandise trade will likely fall between 13 to 32% in 2020. The World Trade Organization (WTO) expects a recovery in trade in 2021, although the extent is likely to be limited. However, trade in agricultural products is projected to contract more significantly, but less than the average across all goods and services. A number of factors suggest that agricultural trade is likely to be less affected than total merchandise trade.

First, demand for agricultural products is relatively income-inelastic; food is an essential product for all, and the options for import substitution, i.e. replacing food imports through domestic production, are limited at least in the short term. Second, a considerable amount of agricultural trade (especially cereals and products in the oilseed complex) takes place in bulk shipments, highly capital-intensive, and trade logistics in many routes are highly automatized with little human interaction. Disruptions due to health reasons are no doubt possible, but they are less likely to result in protracted interruptions of trade flows. For high value perishables (e.g. fruit and vegetables, livestock and fishery products) as well as processed foods, where bulk shipments play a lesser role, the impacts of COVID-19 are expected to be more pronounced, and could lead to a supply-induced worsening of nutritional outcomes, notwithstanding falling incomes of consumers, who may no longer be in a position to afford such foodstuffs. Third, while global food value chains are also becoming increasingly complex, the international division of labour in food and agriculture is much less pronounced than in other sectors. Finally, international prices of food have begun to decline, and this is a sector that has limited recourse to widespread trade restricting measures, such as export bans or taxes.

A global food crisis or not?

The analysis presented in this special feature suggests that a COVID-19-induced global food crisis is not on the horizon. Indeed, while the world food economy was ill-prepared for the shocks that characterized the global food crisis in 2007/08 and the recession that followed in 2009, this cannot be said of the situation in 2020. Global food production prospects are positive, stocks are high, international food prices are low, trade is broader based with more importing and exporting countries, costs of bulk transportation are depressed, fertilizer and input prices remain stable, energy prices have collapsed and competition from biofuels has virtually seized. Policy-makers in 2020 are more experienced in dealing with global crises, and arguably also better informed and better prepared. In high-income countries, central banks are now fully familiar with the instruments of monetary easing; they have been adding new instruments to accommodate additional credit needs. On the fiscal side, governments have been lifting spending constraints. However, the large accumulation of debts in low-income countries, including in foreign currencies, is of concern as it could spark a credit crunch and result in debt defaults.

The importance of ‘global stabilizers’ – allowing market forces to equilibrate imbalances – are key to solidifying the fundamentals for international food security. In order for these stabilizers to do their job, the current hindrances to logistics and distribution must be addressed and mitigated. In this regard, governments must recognize the importance of ensuring that trade, whether internal or international, remains open and frictionless, free from restrictions, and meets food capacities in terms of volumes and fulfilling nutritional gaps. This also implies speedy clearances at customs, borders and ports. The truism that food is the most fundamental need requires that farmers and agricultural workers are placed on the same footing as health workers engaged in fighting COVID-19. Equally, global and national food systems should be regarded as on a par with health systems in ensuring that hunger and poor nutrition problems are not allowed to escalate. This in turn requires that farmers maintain and invest in productivity, with access to affordable credit, and that consumers have normal opportunities to procure food and meet their nutritional needs on the marketplace. Not all countries have the fiscal means to manage the impacts of the pandemic, especially SIDS, which are highly dependent on food imports. Also vulnerable are localized shock-prone countries in sub-Saharan Africa, which are in the grip of other crises, such as pest and disease outbreaks (locust, African swine fever), adverse weather conditions, or compromised security (civil strife). Their societies are facing a loss of income-earning opportunities as well as deepening threats to their livelihoods. As a result, cooperative international support and interventions will be imperative to safeguard the vulnerable populations of these countries and avoid an aggravation of their food insecurity.

[Ed. Note: This article was contributed by Josef Schmidhuber and he can be contacted at Josef.Schmidhuber@fao.org ]

Share This Article: